While AI and geopolitical risks dominate the market narrative, we continue to closely track a more traditional driver of the economic cycle: the labor market.

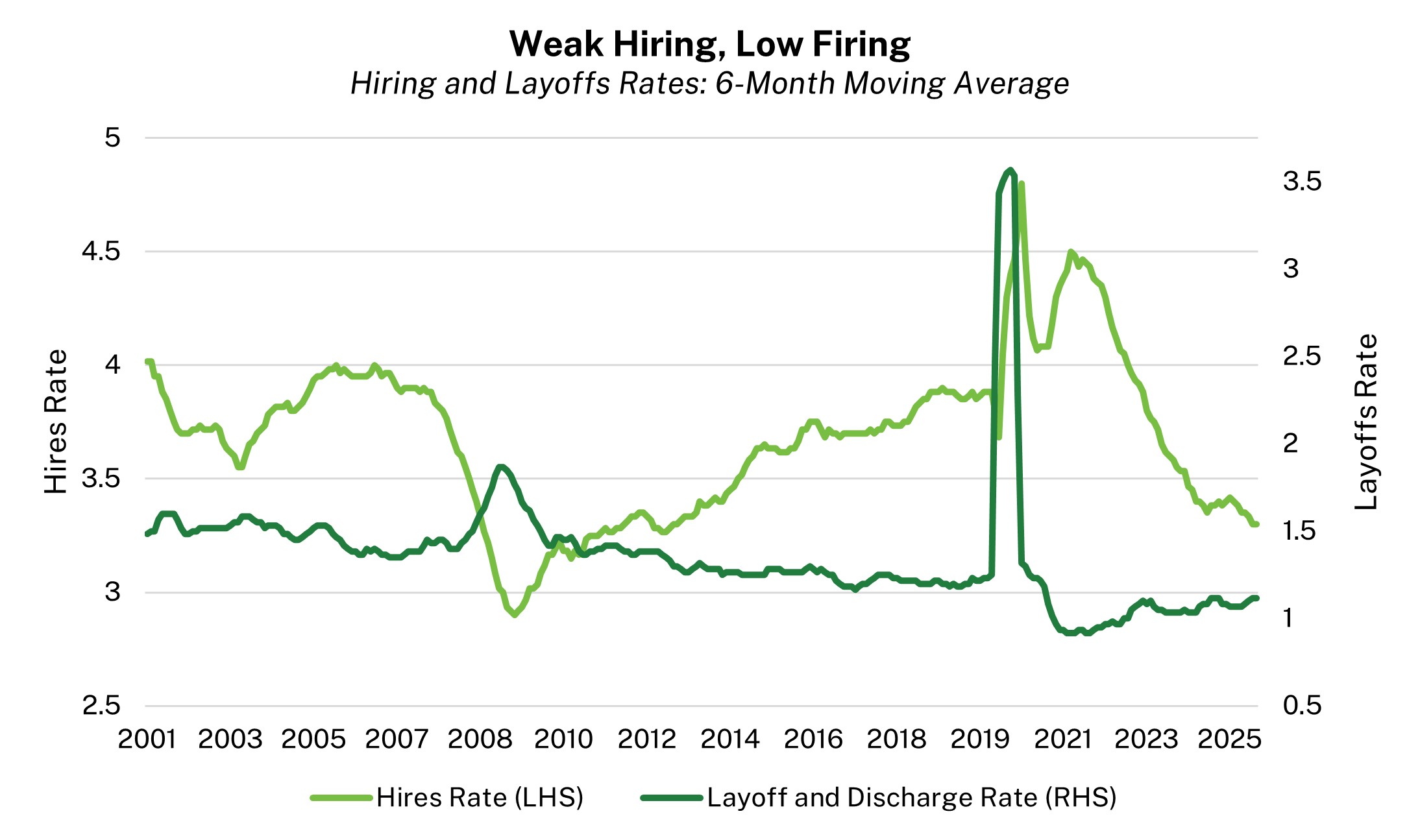

For roughly two years, the labor market has operated in a low-hiring, low-firing environment. Companies are not laying workers off at an elevated pace, but they have also been hesitant to add new employees. Labor supply growth has slowed alongside this reduction in labor demand, in what Fed Chairman Jerome Powell referred to as “a curious kind of balance.”

This is a delicate balance to maintain, and a relatively small move in either supply or demand could have meaningful implications for consumer spending and economic growth.

Structural and Cyclical Drags on Labor Supply

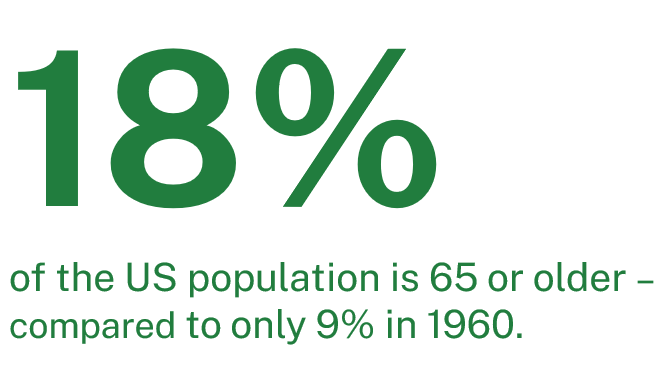

For many years now, an aging population has been a steady and gradual drag on labor force growth as large cohorts of workers reach retirement.

Analysis: Manning & Napier. Source: Federal Reserve Bank of St. Louis (01/01/1960 – 01/01/2024).

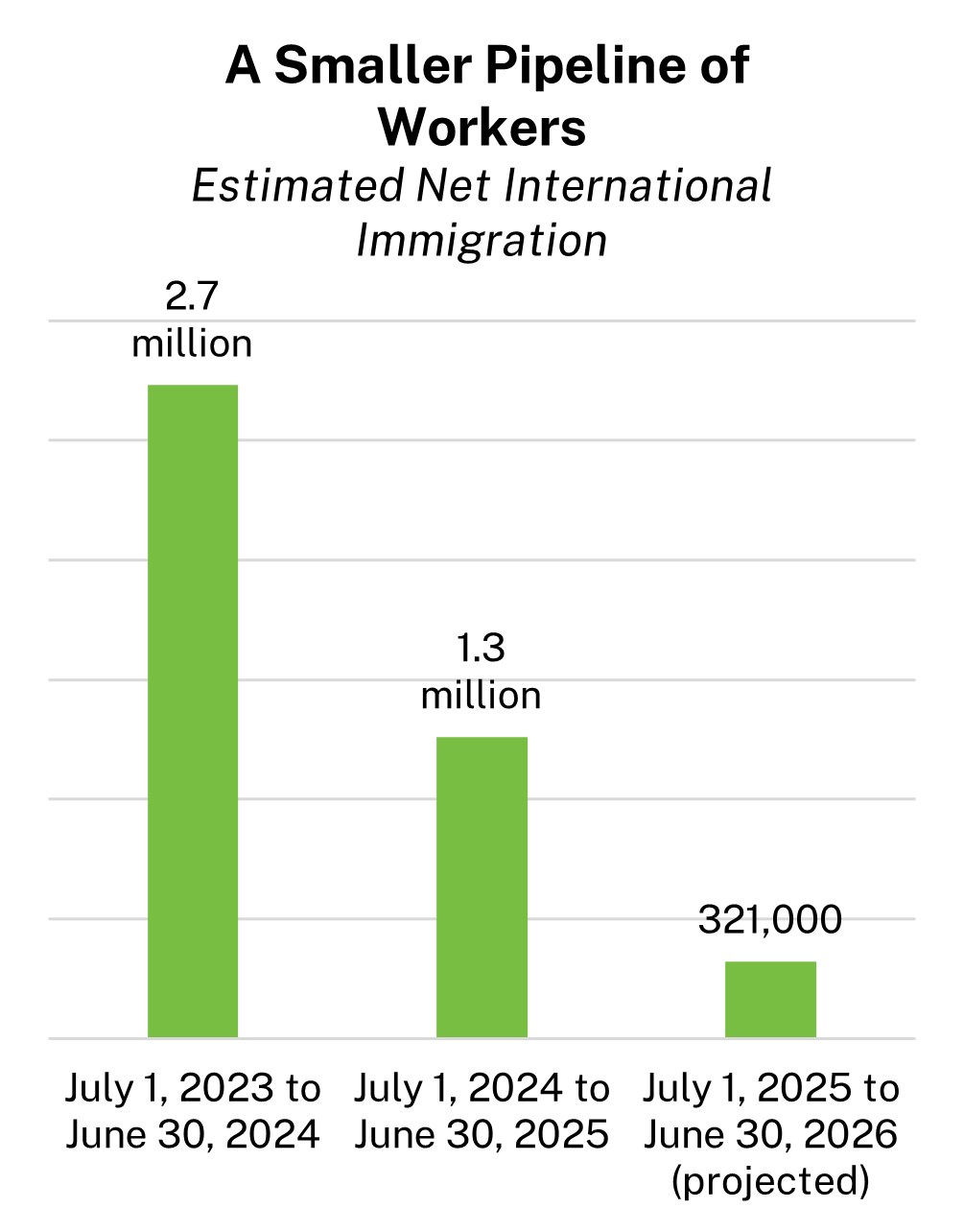

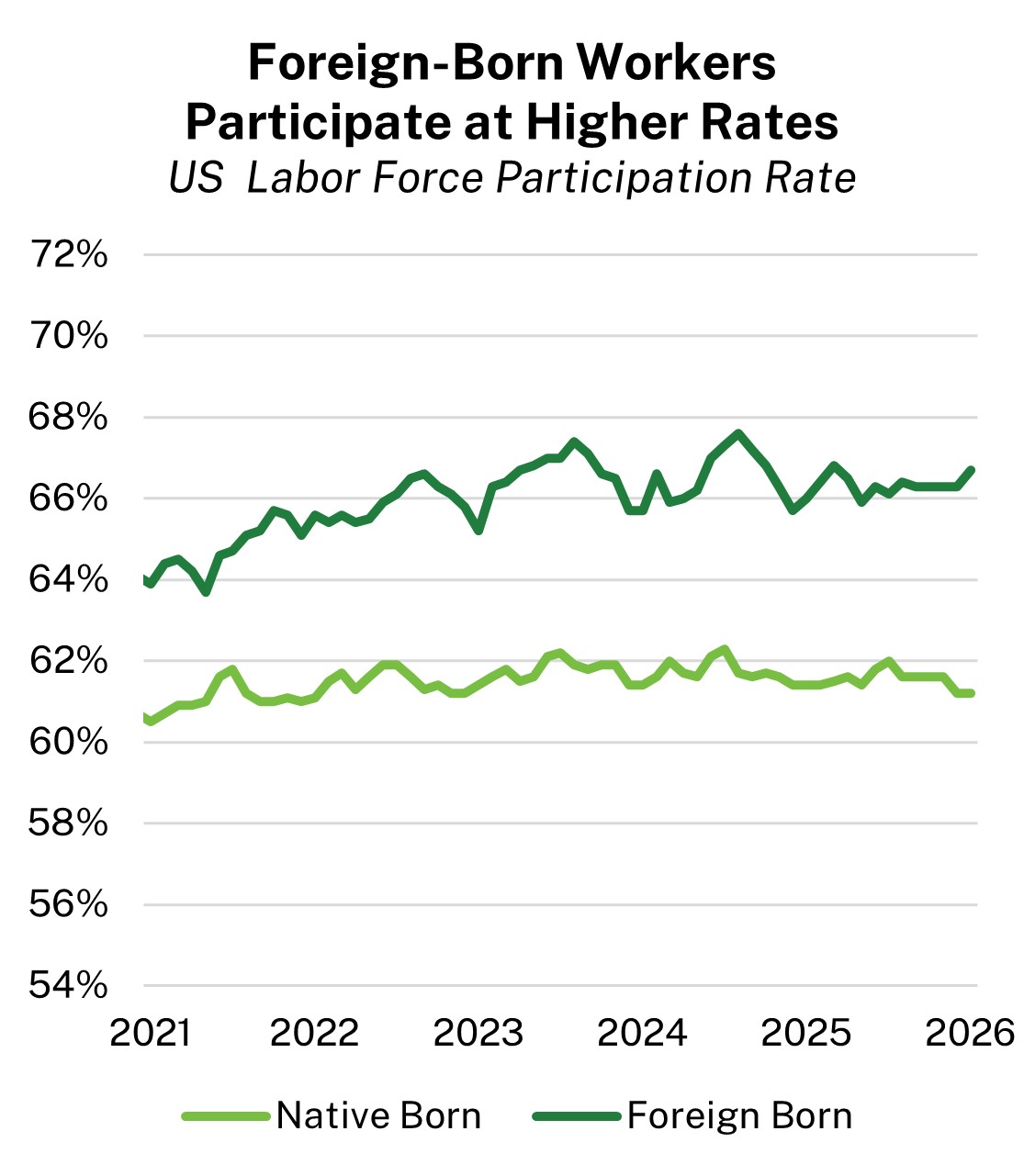

More recently, a steep decline in immigration has put further downward pressure on labor force growth. Immigration has been a meaningful contributor to labor force growth, both as an offset to demographic aging and because foreign‑born workers tend to participate in the labor force at relatively high rates.

Analysis: Manning & Napier. Source: Census.gov (01/01/2023 – 06/30/2026 projected).

Analysis: Manning & Napier. Source: US Bureau of Labor Statistics (12/31/2021 – 01/31/2026).

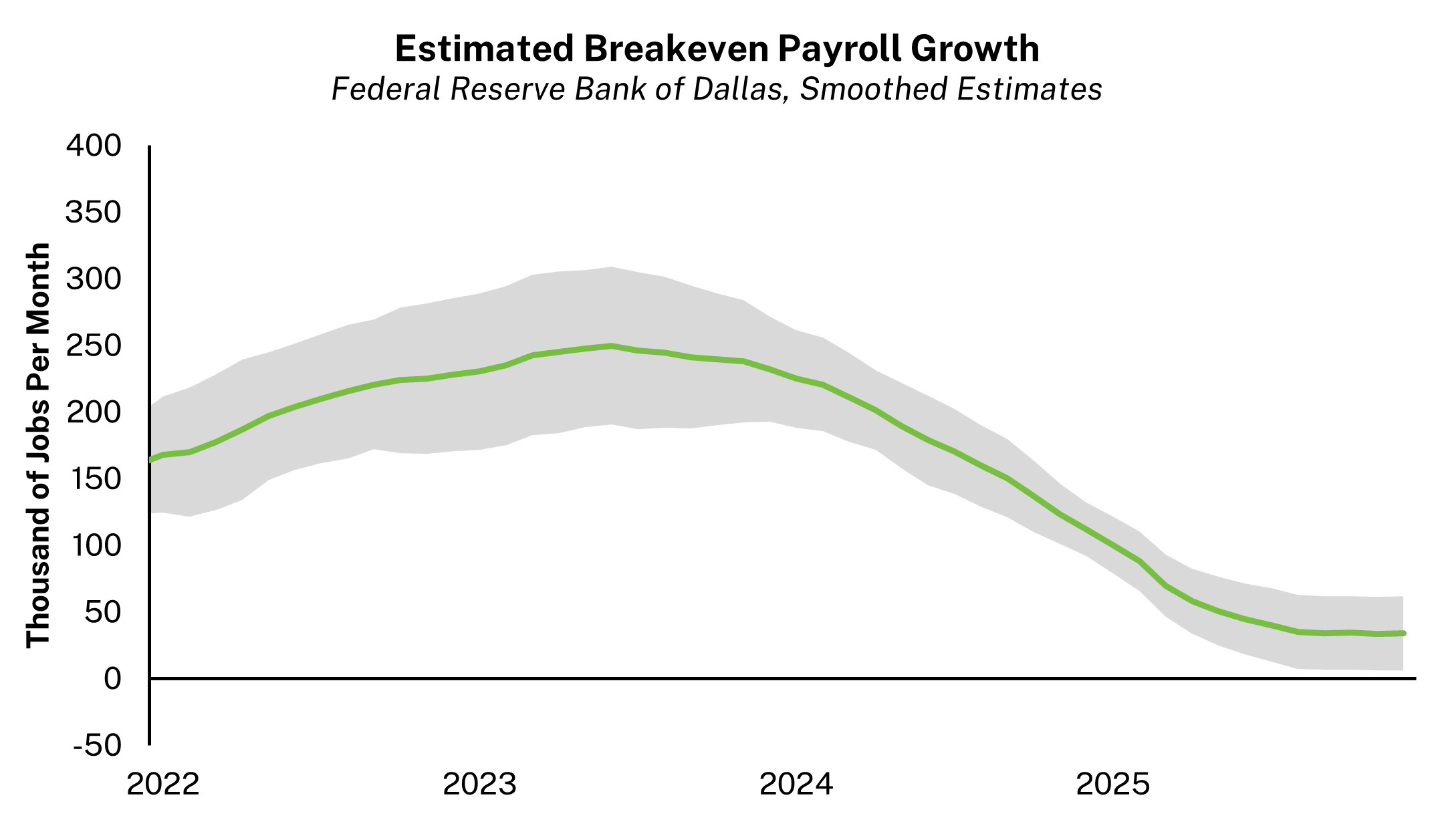

Fewer workers entering the labor force means that fewer jobs are required to keep the unemployment rate constant. This concept is known as the “breakeven” rate of employment growth—the pace of monthly job gains needed to absorb new entrants to the labor force without pushing unemployment higher. While the breakeven rate cannot be observed directly, estimates from a variety of sources have fallen meaningfully as immigration has declined. An October study from the Federal Reserve Bank of Dallas estimated that the breakeven rate of employment growth had dropped to roughly 30,000 jobs per month in mid-2025, down from a peak of approximately 250,000 in 2023.

Note: Gray area illustrates estimate range.

Sources: Bureau of Labor Statistics; Anton Cheremukhin with Federal Reserve Bank of Dallas.

Labor Demand: Bending but not Breaking?

Labor demand has softened alongside the slowdown in labor supply. This reflects a combination of structural forces (such as demographic aging and lower immigration), technological change (including the adoption of artificial intelligence), and cyclical factors tied to business uncertainty and slower growth. Regardless of the precise mix, the result has been a clear reluctance among firms to expand payrolls.

At the same time, layoffs have remained relatively subdued. The combination of weak hiring and limited firing, in conjunction with slow labor force growth, has allowed job growth to slow without triggering a significant rise in the unemployment rate. The resulting equilibrium, however, is inherently fragile. With hiring already depressed, even a modest increase in layoffs would likely have an outsized impact on unemployment, as displaced workers would face a more challenging environment for finding new jobs. In that sense, today’s “curious balance” offers short‑term stability but leaves the labor market vulnerable to even modest negative shocks.

Analysis: Manning & Napier. Source: US Bureau of Labor Statistics (07/31/2001 – 12/31/2025).

Parsing the Role of AI in Recent Labor Market Weakness

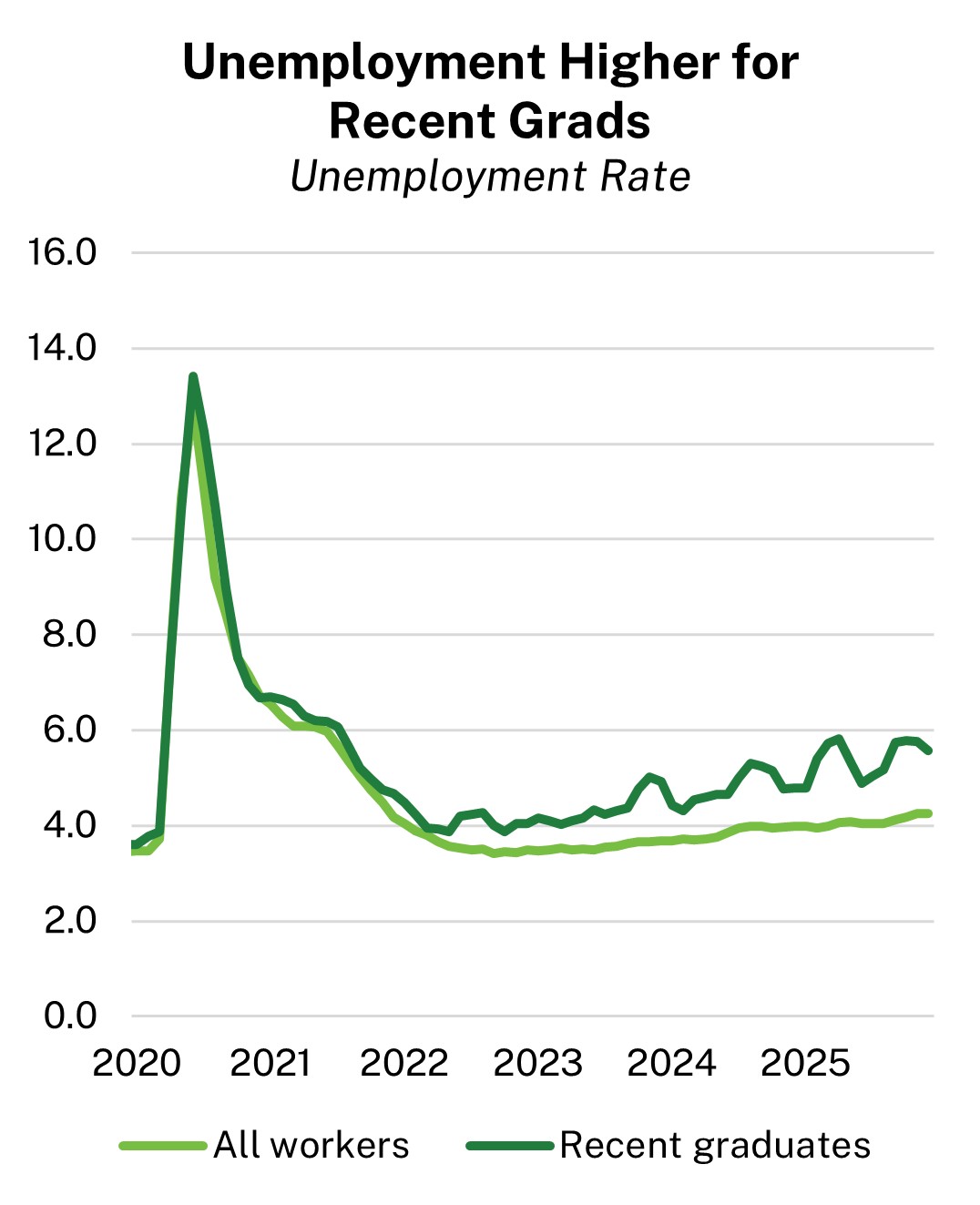

Artificial intelligence has become an increasingly prominent explanation for recent labor‑market weakness, particularly in entry‑level and white‑collar roles. Headlines highlighting elevated unemployment among recent college graduates and well‑publicized layoffs in the tech sector have fueled concerns that AI is already displacing workers at scale. Many of these developments, however, have plausible alternative explanations.

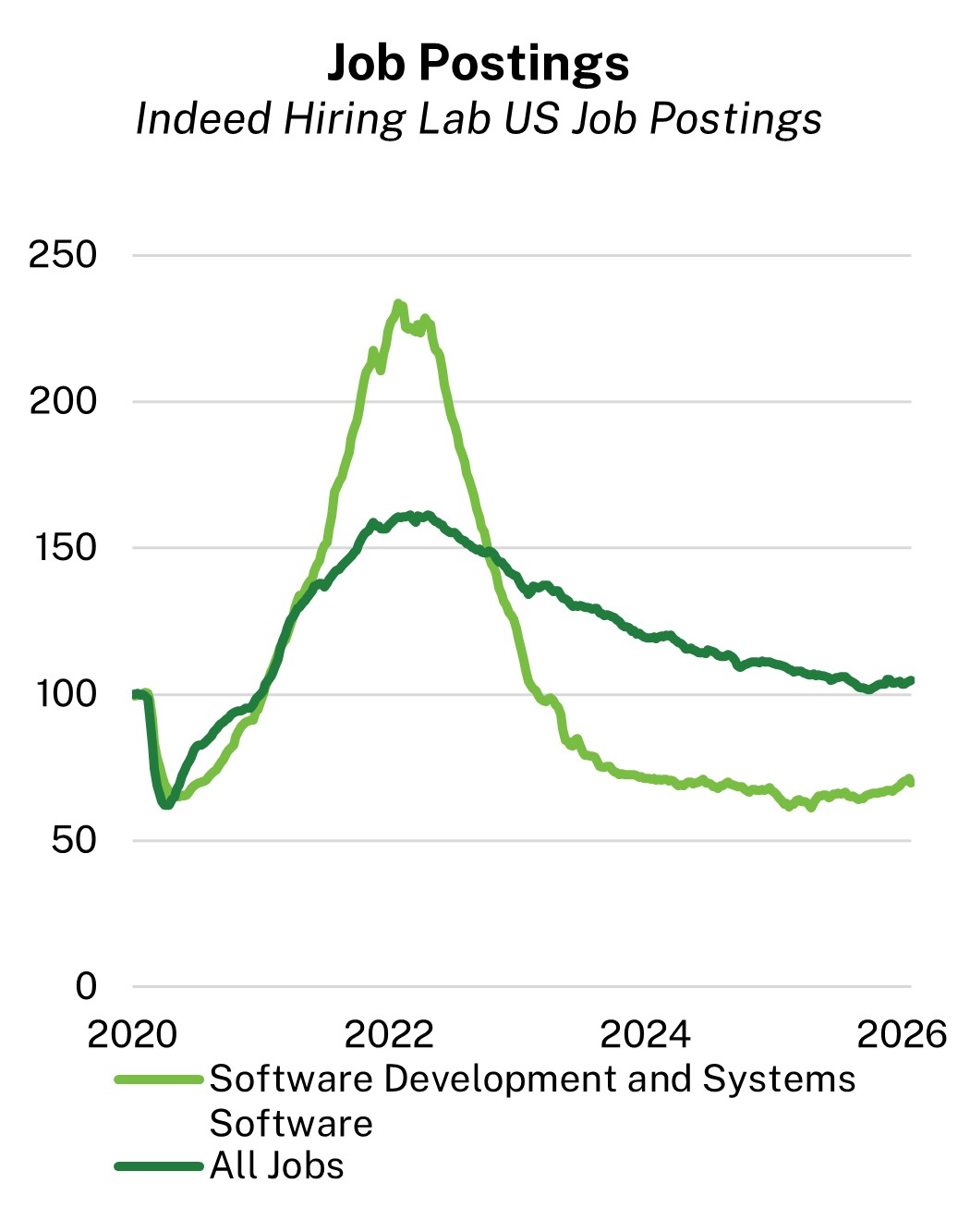

In a low‑hiring, low‑firing environment, it is not surprising for unemployment to rise among new college graduates, who disproportionately need to find new employment even if they have not been laid off from a prior job. Similarly, job cuts in the tech sector follow a period of exceptionally strong hiring and may in part simply reflect a normalization after rapid post-pandemic growth and, for large technology firms in particular, a reallocation of resources toward capital spending as companies invest aggressively to compete in the AI arms race.

US Census Bureau and U.S. Bureau of Labor Statistics, Current Population Survey (IPUMS)

Analysis: Manning & Napier. Source: Federal Reserve Bank of New York (01/01/2020 – 12/01/2025).

US Indeed Hiring Lab Job Postings Index

Analysis: Manning & Napier. Source: Bloomberg (02/02/2020 – 02/27/2026).

It is also important to note that the initial public release of ChatGPT occurred while the Fed was in the midst of an aggressive interest rate hiking campaign. Thus, the timing of labor market weakness that appears to coincide with AI could simply be monetary policy working as intended.

Spending Resilience Amid Labor Market Fragility

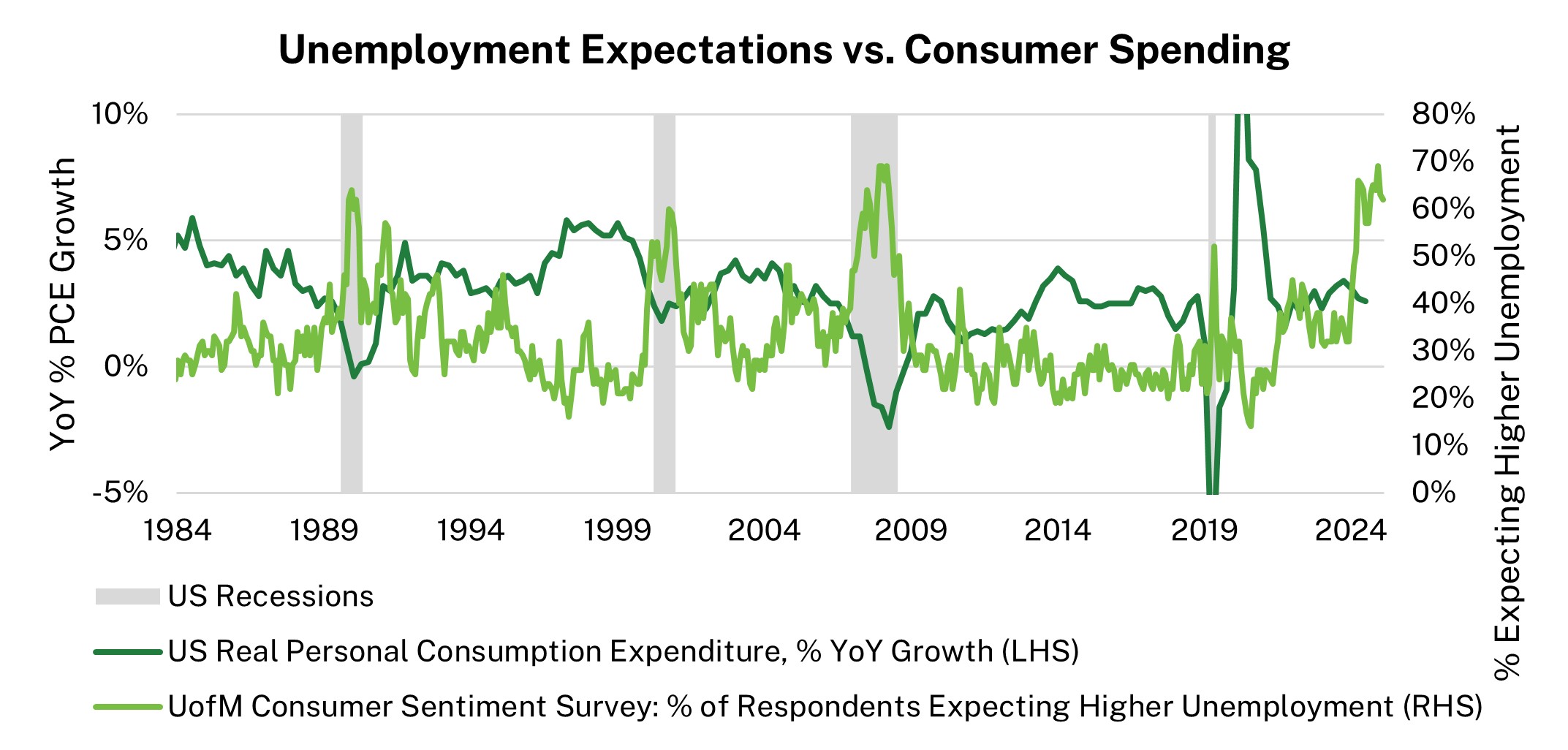

Consumer surveys suggest workers are quite sour on job prospects. Despite viewing job prospects as negatively as they have in recessionary times, spending growth has remained steady.

Analysis: Manning & Napier. Source: Bloomberg (01/31/1984 – 01/31/2026).

This discrepancy may be a result of the low-hiring, low-firing dynamic: workers know that if they lose their job, they will have a hard time finding a new one, but while they remain employed, they are still willing to continue spending.

In this environment, labor market stability is less a function of robust job creation than of limited job destruction. The same low‑hire, low‑fire dynamic that has allowed spending to hold up also increases the economy’s sensitivity to shocks, as displaced workers face fewer opportunities to re‑enter employment. Ultimately, today’s equilibrium depends less on robust hiring and more on the absence of layoffs, a condition that offers limited protection against future shocks.

This material contains the opinions of Manning & Napier Advisors, LLC, which are subject to change based on evolving market and economic conditions. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product.